Hardwood lumber being stacked after processing. / Photo Credit: M. Bumgardner

By Matthew Bumgardner and Scott Bowe

Hardwood lumber production in the United States reached a peak in 1999, with an estimated 12.6 billion board feet of output. However, the early 2000s ushered in a major structural shift – the large-scale offshoring of U.S. furniture manufacturing. Once the single largest user of hardwood lumber until the late 1970s, wood furniture has become the smallest major market for hardwood lumber today.

As U.S. furniture production moved offshore, the industry shifted its focus toward housing and construction markets, which were entering a period of robust growth in the early 2000s. Sectors producing housing fixtures, including cabinets, flooring and millwork, all saw strong demand during this period. This bolstered demand for the higher value “appearance grades” of hardwood lumber. However, the housing market crash came in 2007-2008, which remains the single most significant disruption to the hardwood industry in recent history. The crisis profoundly reduced demand for many hardwood products.

The Impacts

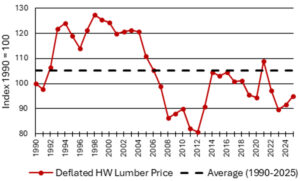

Annual inflation-adjusted hardwood lumber price index. / Data: Bureau of Labor Statistics

The combined impacts of lower demand from furniture manufacturers, and then from housing-based markets, are evident in many ways. For example, the number of hardwood sawmills has steadily declined since 2005. Hardwood lumber production hit a deep low point in 2009 and was even lower in 2025. Since 2006, the annual inflation-adjusted aggregate price of hardwood lumber has risen above the long-term average just once (in 2021). Employment in secondary sectors such as kitchen cabinets and millwork, which are correlated with single family housing starts, also have seen dramatic declines. During the worst years of the housing crisis, the value of single-family housing construction dropped below that of residential remodeling spending from 2009 to 2011, partially because foreclosed homes required maintenance to become marketable but also because the drop in single-family housing construction was so severe.

Exports

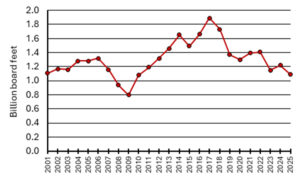

U.S. hardwood lumber exports. / Data: USDA Foreign Agricultural Service

As demand for appearance-grade hardwood lumber waned during the housing crisis, exports were a lifeline for the industry. This market shift created a new level of connectedness for U.S. sawmills with global economic trends. China emerged as the most significant market in this new era; its share of U.S. hardwood lumber export volume surged from 19 percent in 2008 to 54 percent in 2017. By 2017, China accounted for $1.5 billion of the $2.6 billion in total U.S. hardwood lumber exports. However, hardwood lumber exports peaked at 1.9 billion board feet in 2017 and dropped to 1.1 billion board feet by 2025, a decline of 42 percent. Much like the rise, the decline was largely a result of lower shipments to China, resulting from both trade disputes and lower demand as the Chinese economy slowed. Despite the decline in demand from China, it remains the single largest destination. U.S. hardwoods remain sought after in many foreign markets.

Industrial Markets

Another critical change over the last quarter-century has been the increased relative importance of industrial markets to hardwood lumber demand. Industrial products include pallets, containers and railway ties, and tend to use lower grade and/or lower value hardwood lumber. In the absence of strong furniture and housing markets, these industrial sectors have become the largest domestic consumers of hardwood lumber. By 2014, industrial products accounted for 51% of total hardwood lumber consumption, up from 39% in 2002. While industrial markets are critical to the industry’s need to find markets for all parts of the sawlog, a prolonged shift to lower grade products has implications throughout the hardwood supply chain and ultimately could impact the value of the hardwood resource. The industry also faces challenges in industrial markets, including a shift to softwood lumber use in pallet manufacturing.

Current Challenges

The last five years have introduced a new set of challenges for the hardwood industry. The industry faced another significant downturn in 2020 due to COVID-19 disruptions. While the market briefly recovered, demand for hardwood lumber has declined further since 2022. This decline resulted from several factors, including slowing global demand, a cooling housing market and competition from substitute materials that have gained market share in several hardwood sectors. For example, substitute products including luxury vinyl tile (LVT) and luxury vinyl plank (LVP) have gained market share from hardwood flooring. Advancements in technology have allowed these products to mimic the appearance of hardwood at a lower price point. While research suggests consumers value many of the attributes of solid hardwoods, the industry must devise ways to offset the higher cost in the minds of consumers. Consumer markets also are becoming increasingly customized, which offers opportunities to promote the attributes of different hardwood species.

Conclusion

Today, the hardwood industry is leaner and more globalized than when it entered the 21st century. The past 25 years have proven the industry’s overall resilience. Going forward, its future depends on navigating a business environment where global trade, macroeconomic trends, marketing and industrial efficiency are more interwoven than ever before.

Matthew Bumgardner is a Research Forest Products Technologist with the USDA Forest Service, Forest Products Laboratory (Matthew.Bumgardner@usda.gov) and Scott Bowe is a Professor of Wood Products with the University of Wisconsin (SBowe@wisc.edu).